For property and casualty insurers, pricing has always been complex. But the conditions now reshaping that complexity are fundamentally different from anything the industry has faced before.

Inflation continues to drive loss costs higher and faster than traditional pricing cycles can absorb. Catastrophic events are becoming more frequent and severe, rendering pricing assumptions outdated faster than ever. Reinsurance costs have risen significantly, yet many carriers still lack the exposure visibility needed to negotiate effectively. And policyholders are shopping at unprecedented rates — personal auto policy shopping reached historic highs in the fourth quarter of 2025, with nearly half of all policies shopped at least once in the prior 12 months.

These pressures were at the center of ValueMomentum’s recent webinar, “How to Get Pricing Modernization Right From the Start,” where I spoke with Karlyn Carnahan of Celent and Drew Lawyer of Earnix to explore what it actually takes for P&C carriers to modernize pricing effectively.

The Problem Is Structural

Many carriers have evolved their pricing environments incrementally, shaped by new product launches, acquisitions, and regulatory requirements. The result is a familiar structural pattern: actuarial modeling, rating execution, and operational deployment exist in separate silos with limited integration between them. Actuaries and product specialists remain heavily dependent on IT to implement pricing changes, and what should take days can stretch into months. By the time a rate change reaches the market, the conditions that prompted it may have already shifted.

This structural disconnect has real consequences: pricing leakage, eroding profitability, and reactive decision-making. Underwriters face fragmented systems, manual processes, and siloed tools that slow decisions and introduce inconsistencies, widening the gap between what actuaries intended and what reaches the market.

Addressing this requires a different kind of ambition. As Karlyn shared, “The carriers that are seeing the real impact are the ones that treat this as a combination of three things working together: a clear platform strategy that supports the modern capabilities; an integration approach that connects actuarial, rating, underwriting, and data systems; and an operating model vision that defines how pricing actually gets it done across the enterprise.”

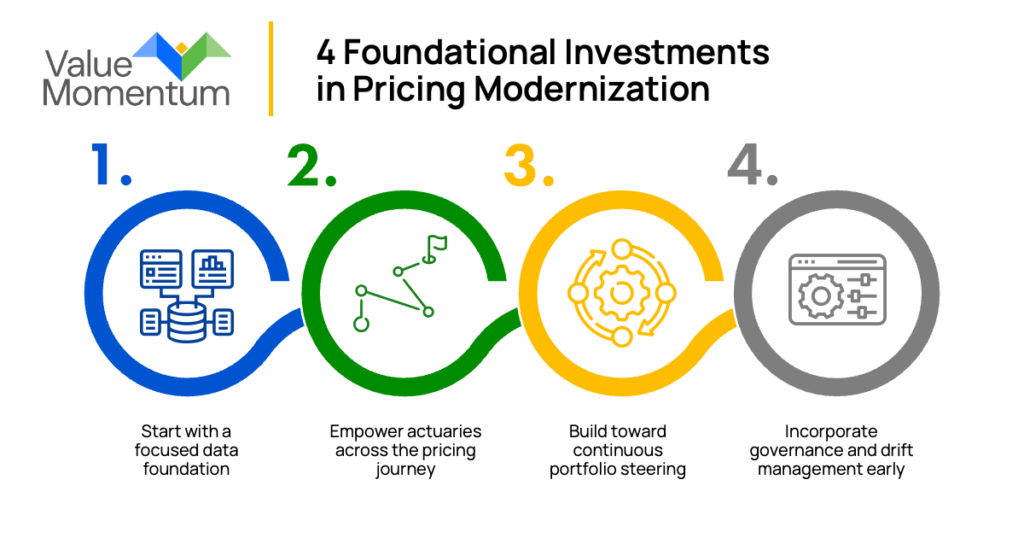

What Pricing Modernization Looks Like in Practice

Getting pricing modernization right requires both a clear vision and a disciplined execution path. The operating model is the “why.” It defines the future state of the pricing organization, determining how actuarial, underwriting, IT, and operations work together. The operating model should also house the governance structures that keep modernization on track.

But a refined operating model alone does not move the business forward. The “how” is where carriers either accelerate or stall, and it depends on making the right foundational investments in the right sequence.

1. Start With a Focused Data Foundation

The instinct is often to pursue comprehensiveness — to ingest every available data element before moving forward. In practice, carriers who are seeing results most quickly take a more focused approach. Drew explained, “Focus on that core feature set; it’s usually between 20 to 40 pieces of input. Build out that repeatable process and then start building from there.” Identifying the data elements that drive the most predictive value, ensuring those can be operationalized reliably, and building repeatable processes around them before expanding further shifts the data function from an academic exercise into an operational one.

2. Empower Actuaries Across the Pricing Journey

The traditional approach, where actuarial teams develop pricing logic and hand it off sequentially to IT, audit, and filing functions, introduces compounding delays and disconnect at every stage. Leading carriers are replacing this with a governed, end-to-end workflow where rate, rule, and product changes move through a streamlined process with clear ownership and fewer handoffs, resulting in faster deployment cycles; fewer errors; and a tighter connection between what was modeled, what was filed, and what was deployed.

3. Build Toward Continuous Portfolio Steering

Carriers that can continuously sense market conditions, run scenario models in near-real time, and feed those signals back into pricing and underwriting decisions are operating at a fundamentally different level than those still running annual or biannual pricing cycles. This continuous feedback loop, which connects market inputs to pricing outputs to portfolio performance, is what separates carriers that proactively shape their book from those that react to it after the fact. Carriers today have an opportunity to bring these elements together and operationalize them. It requires governance, change management, and a disciplined operating model design.

4. Incorporate Governance and Drift Management Early

Modernization does not end at deployment. Pricing assumptions can become outdated quickly in volatile market conditions, and models that performed well at launch will drift over time without active monitoring. Carriers that treat governance as an ongoing discipline with clear processes for detecting drift and making dynamic adjustments are better positioned to sustain the gains that modernization delivers.

Focusing on these elements can help carriers transform their pricing function from a periodic process to a continuous enterprise capability that directly influences growth, profitability, and market responsiveness. Insurers that invest in deliberately modernizing their pricing capabilities, and in the right sequence, will be poised to stay ahead as markets and risks shift.

Building Pricing as a Long-Term Competitive Capability

Pricing modernization is one of the most complex undertakings a P&C carrier can pursue, and its importance can be deeply misunderstood. Turning pricing into an impactful function does not require being first to adopt a new platform; it takes a clear operating model vision, a deliberately crafted data foundation, and redesigned workflows and matching ownership structures.

Carriers still in the early stages of this journey do not have to modernize every component of their pricing function at once. A well-defined roadmap with the right governance, the right sequence of investments, and a clear three- to five-year vision makes incremental progress both achievable and impactful. Competitive conditions will continue to intensify, and carriers that modernize with clarity and discipline will be better positioned to grow profitably and respond to whatever the market brings next.

To learn more about modernizing pricing and how to respond to changing market conditions, watch ValueMomentum’s on-demand webinar, “How to Get Pricing Modernization Right From the Start.”