Insurance pricing has always been complex. But the conditions property and casualty (P&C) carriers are navigating have raised the stakes considerably. Insured catastrophe losses have exceeded $100 billion globally for five consecutive years, auto insurance rates rose more sharply in early 2024 than at any point since the 1970s, and carriers managed more than 3,300 regulatory updates in 2024 alone.

At the same time, MGAs, insurtechs, and data-driven competitors are deploying rates and products faster than many traditional carriers can match. Pricing risk accurately and deploying rates quickly have become determinants of profitability and market position.

Most carriers know this. But the systems and workflows many rely on were built for a different era. Modernizing pricing and rating is about more than just efficiency; it has become a critical factor in staying competitive.

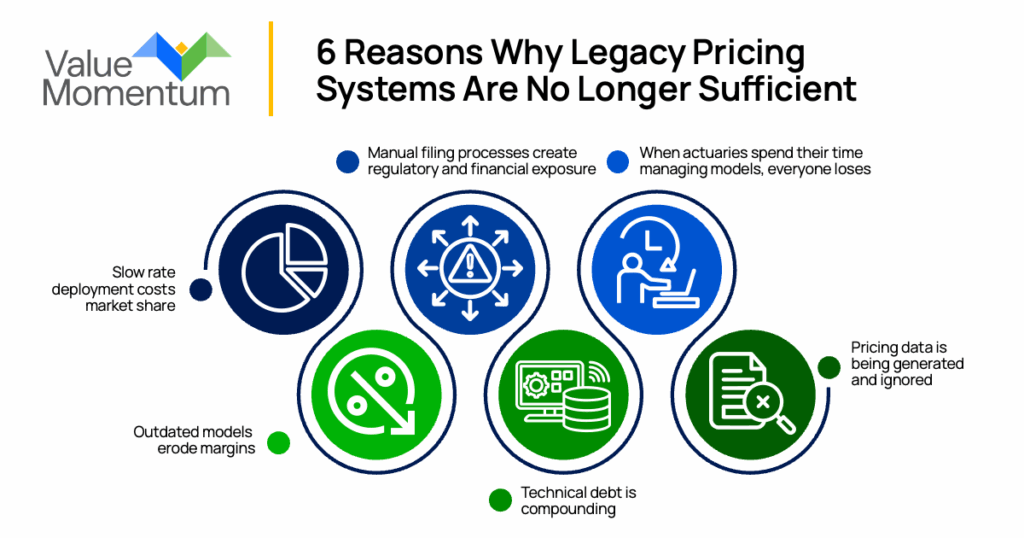

Why Legacy Pricing Systems Are No Longer Sufficient

The gap between what modern markets demand and what legacy pricing environments can deliver is structural. Rating logic embedded in core systems, actuarial workflows dependent on manual handoffs to IT, disconnected rating engines, and Excel-based models that are difficult to audit or test aren’t isolated inefficiencies.

They are symptoms of a pricing architecture that was never designed for the speed, transparency, or data accessibility that competitive pricing now requires.

Here are six reasons why closing that gap has become urgent.

1. Slow rate deployment costs market share.

For most carriers operating on legacy pricing environments, a meaningful rate change can take months to move from actuarial concept to deployed rate. That timeline reflects pricing logic embedded in core systems, IT queues that prioritize stability over speed, and manual testing cycles that can’t be compressed without introducing risk. It is a widely recognized problem: 41% of actuaries say making changes to applications and processes takes far too long. By the time a new rate is live, the loss environment it was designed to address may have already shifted.

Carriers that can deploy rate changes in days rather than months are better positioned to respond to emerging loss trends, exit unprofitable segments faster, and capture market share when conditions favor growth. Those operating on legacy cycles are, by definition, pricing yesterday’s risk at today’s rates, and that gap increasingly shows up in combined ratios.

When actuarial teams can model, test, and deploy rate changes independently, without IT translation cycles, the pricing function becomes a genuine lever for profitability rather than a lagging indicator of it.

2. Outdated models erode margins.

Pricing accuracy depends on models that reflect current loss conditions. When those models are updated infrequently, or when the data feeding them is incomplete, stale, or fragmented across disconnected systems, carriers end up underpricing risks they don’t fully understand. The consequences show up in loss ratios.

Social inflation, for example, has driven significant reserve additions in recent years, with analysts noting that insurers are still struggling to price accurately for this persistent trend. The hard market of the past several years provided cover for many carriers. Broad rate increases lifted results even where pricing sophistication was limited.

As that market softens, carriers need the granular segmentation and continuous modeling capabilities to price individual risks accurately, not just lines of business in aggregate. Carriers relying on periodic model refreshes and manual data workflows will find it increasingly difficult to maintain rate adequacy as conditions shift.

3. Manual filing processes create regulatory and financial exposure.

Rate filing is one of the most compliance-intensive functions in insurance, and one of the most vulnerable to manual errors. Each state maintains its own filing requirements, approval timelines, and documentation standards. Carriers operating across multiple states must navigate them all simultaneously. The volume and complexity of regulatory updates continue to grow, with increased scrutiny around pricing transparency, consumer protection, and data governance adding to the compliance burden. This makes it increasingly difficult for pricing teams to avoid introducing errors.

According to the Earnix 2024 Industry Trends Report, almost 50% of insurers surveyed had incurred regulatory fines or been required to issue refunds due to filing errors, with some carriers losing hundreds of thousands or even millions of dollars annually as a result. Beyond fines, filing errors introduce delays that slow rate deployment.

A filing that requires resubmission or additional regulatory back-and-forth can set a carrier’s go-to-market timeline back by weeks or months. Modern pricing platforms address this by linking pricing models, production rating logic, and regulatory filing documentation in a single governed environment, ensuring consistency between what is modeled, what is filed, and what is deployed. This ensures that what is filed reflects what is actually in production, with a clear audit trail supporting both regulatory review and internal governance.

4. Technical debt is compounding.

Most carriers arrived at their current pricing architecture incrementally — adding a rating engine for a new line of business here, maintaining an Excel-based model for a legacy product there, and patching core systems rather than replacing them. The result, for many, is a fragmented pricing environment in which multiple disconnected rating engines operate in parallel, each with its own logic, maintenance requirements, and compliance risks.

The scale of this problem is significant: HFS Research estimates the insurance industry is carrying $200 billion in combined technology and process debt. In 2024, nearly 80% of business and technology leaders in insurance and financial services reported technical debt had caused cancellation of business-critical projects, organizational paralysis, and increased costs.

The fragmented pricing environments many carriers have, spanning multiple rating engines and spreadsheet-based models for varying lines of business, are difficult to audit, challenging to test systematically, and prone to version-control failures that can introduce errors quietly and at scale. Every workaround added to accommodate legacy systems makes the next change harder. Each year a modernization project is deferred, the pricing architecture becomes more complex, more dependent on institutional knowledge, and more costly to modernize.

5. When actuaries spend their time managing models, everyone loses.

Actuaries are among the most expensive and specialized talent a carrier employs. They are also, at many carriers, among the most underutilized. When pricing teams are built on legacy infrastructure, the bulk of an actuary’s time is spent on maintenance rather than analysis. And the work that really requires actuarial judgment, such as refining segmentation, identifying emerging loss trends, and stress-testing rate adequacy, gets compressed into whatever time is left over.

Paying for strategic capability and deploying it on operational maintenance is a misallocation that compounds over time as models age, data pipelines drift, and the backlog of meaningful analytical work grows. The gap between what actuarial teams can do and what legacy infrastructure allows them to do is not a people problem; it is an architecture problem.

There is also a talent dimension that carriers increasingly cannot afford to ignore. Experienced pricing actuaries have options, and the quality of the tools they work with factors into where they build their careers. Legacy environments that force skilled professionals to spend their days on data reconciliation and manual validation make it harder to attract and retain analytically sophisticated talent.

6. Pricing data is being generated and ignored.

Every quote a carrier writes contains information: how a risk was described, how it was priced, whether it was bound, and what it ultimately cost. The feedback loop that should connect pricing outcomes back to pricing assumptions is, for most carriers, either broken or nonexistent. It sits in spreadsheets, gets reconciled manually at quarter-end (if at all), and disappears into a reporting cycle that is too slow and too coarse to influence day-to-day pricing decisions.

Carriers without functioning data feedback loops are making pricing decisions on historical models that don’t reflect current experience. They may not know which segments are underpriced until loss ratios confirm it months later. They can’t identify which rate changes actually improved profitability and which ones didn’t. And as competitors increasingly deploy pricing environments that capture and act on real-time quote and bind data, carriers still operating on quarterly model refreshes are at a structural information disadvantage.

A pricing environment that captures every quote, feeds outcomes back into models continuously, and integrates both internal and third-party data sources improves over time. Each cycle produces better segmentation, more accurate loss predictions, and pricing decisions grounded in the portfolio rather than what happened two quarters ago.

As these six reasons show, legacy pricing environments are not just operationally inefficient; they are strategically limiting, and the gap between what carriers can do today and what the market demands is widening.

The Cost of Waiting Is Already Being Paid

Speed, margin integrity, regulatory compliance, technical debt, actuarial capacity, and data utilization aren’t separate problems. They are interconnected symptoms of the same underlying gap. Addressing them in isolation yields diminishing returns.

The window to act with intention is narrowing. MGAs, insurtechs, and data-driven competitors are already deploying these capabilities. Carriers that move deliberately will be better positioned to price risk accurately, respond to market shifts quickly, and build the kind of pricing function that sustains profitable growth.

To learn more about how leading insurers are modernizing their approach to pricing and underwriting, watch our on-demand webinar, “AI Insider Insights: How Leading Insurers Are Transforming Underwriting with AI.”