For P&C insurers, pricing and rating sit at the center of nearly every strategic decision — from how risk is selected and priced to how quickly new products reach the market. But legacy pricing systems leave insurers with rate cycles measured in months, actuarial teams buried in spreadsheet maintenance, and limited visibility into whether pricing decisions are performing in the market.

According to the Earnix 2024 Industry Trends Report, 70% of annual insurance IT budgets go toward legacy system maintenance, keeping these resources from powering modernization and growth initiatives. However, while replacing a legacy rater with a modern platform is necessary, it is not sufficient.

Insurance pricing modernization that delivers lasting business agility requires building an interconnected ecosystem of capabilities spanning rating execution, integration, analytics, and governance — and doing so in a sequence that reduces risk while accelerating time to value.

What a Modern Pricing and Rating Ecosystem Looks Like

The modern pricing and rating ecosystem spans multiple layers, from data infrastructure to rating execution and portfolio monitoring. At the implementation level, several capabilities are foundational to making it work in practice.

The first is business-led pricing enablement. A modern insurance pricing and rating environment enables actuarial and pricing teams to create, test, and deploy rate changes directly, eliminating the need to go through IT for every change. Equally important is a reusable, consistent pricing integration framework. A centralized, API-driven integration layer standardizes how pricing requests and responses flow between the pricing platform and downstream systems, eliminating point-to-point integrations and enabling consistent rating execution across the enterprise.

End-to-end pricing traceability and actuary-owned test automation address the governance dimension. Automated regression testing driven by actuarial teams, rather than IT, enables safe and frequent releases without creating dependency on engineering cycles. Controlled migration from legacy raters is also essential. Most carriers operate multiple rating systems in parallel. A phased migration approach, supported by parallel runs and automated rate-matching validation, ensures the target platform produces outputs that match legacy logic before cutover, reducing risk and building actuarial confidence in the new environment.

Insurance pricing modernization must also include an analytics foundation that enables continuous validation and improvement. Market impact visibility and real-time feedback loops allow teams to monitor whether deployed rates are delivering intended outcomes across loss ratio, retention, and new business growth, as well as to refine models continuously as performance data accumulates. These capabilities give actuaries the confidence to model with precision, deploy with governance, and course-correct with data rather than intuition.

The question for most carriers is not whether to build these capabilities, but how to do so in a way that delivers early value without creating new technical debt.

A Phased Approach to Pricing and Rating Transformation

Pricing and rating modernization is not a single project with a defined end state. It is a multi-phase transformation that builds capability incrementally, with each phase creating the foundation for the next.

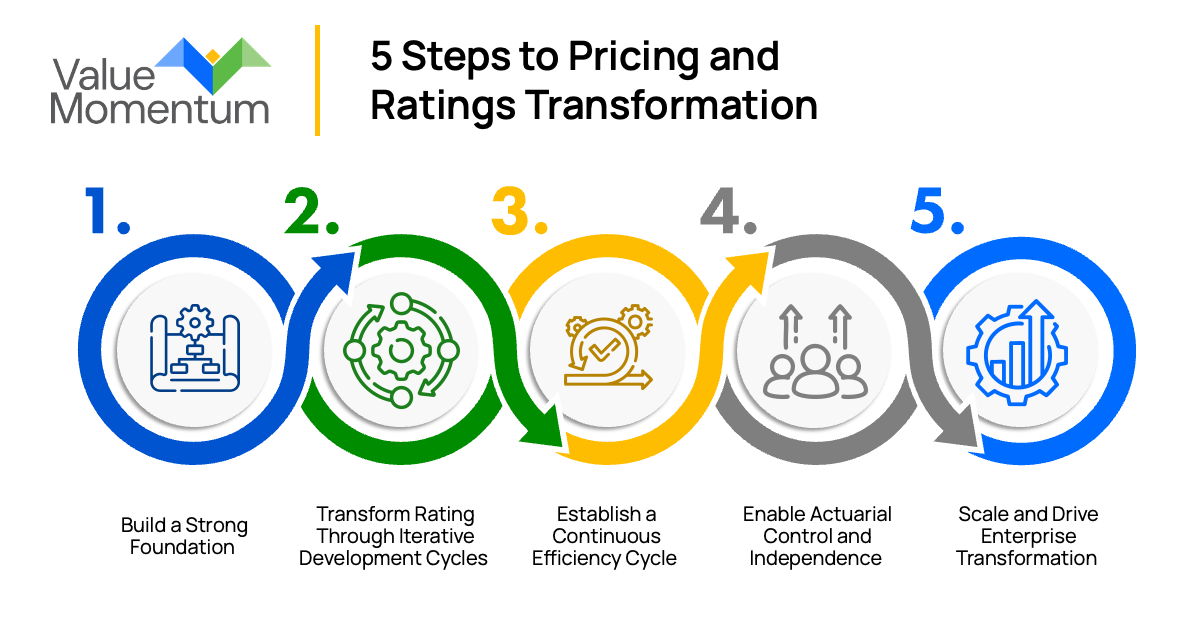

The following five-step approach reflects the sequence that consistently delivers results across carriers of varying size, complexity, and pricing maturity.

1. Build a Strong Foundation

Before any migration or platform work begins, carriers need a clear picture of what they are working with. As a result, they must conduct a thorough inventory of existing rating logic across all systems, establishing a robust data foundation that includes the full range of variables actuaries need for modeling and prioritizing the work ahead based on complexity, business impact, and reusability.

Discovery is not a formality; it is the phase that determines whether the transformation that follows is grounded in reality or built on assumptions that will unravel later. Carriers that invest in a rigorous foundation phase consistently report fewer surprises, shorter delivery cycles, and better outcomes in subsequent phases.

2. Transform Rating Through Iterative Development Cycles

Rather than attempting a single large migration, leading carriers modernize rating incrementally, working through analyze, plan, build, validate, and deploy cycles that produce production-ready capabilities at the end of each iteration.

Each cycle builds on the last, drawing on accurate data, simulation environments, and rigorous regression testing to ensure migrated logic matches legacy outputs before cutover. This iterative approach reduces risk, surfaces issues early, and keeps stakeholders aligned throughout the program rather than discovering gaps at go-live.

3. Establish a Continuous Efficiency Cycle

As the program matures, carriers can accelerate delivery by building and reusing shared assets, such as rating patterns and algorithms, common integration APIs, configuration templates, and automated regression test suites. These accelerators reduce the time and cost of each subsequent iteration and shift the program from bespoke delivery toward a standardized, repeatable model.

The efficiency gained in later cycles is what makes it possible to expand across additional lines of business and states without proportionally expanding the team or the timeline.

4. Enable Actuarial Control and Independence

The goal of pricing and rating modernization is not only to achieve a faster rating engine but also to fundamentally shift how the pricing function operates. When pricing logic is externalized from core systems and actuaries can configure, simulate, and deploy rate changes without IT involvement, the pricing function gains the agility it needs to respond to market conditions in real time.

Data-driven modeling environments, scenario analysis capabilities, and reduced IT dependency are the operating model that modern pricing requires.

5. Scale and Drive Enterprise Transformation

Once the foundational capabilities are in place and the operating model is established, carriers can expand across products, states, and channels using the standardized frameworks and reusable components built in earlier phases. Performance analytics feed continuous improvement, rapid rollouts become achievable without proportional increases in delivery risk, and the pricing function becomes a competitive advantage.

Each phase builds capability along with the organizational muscle to use that capability well. That combination is what determines how far the transformation ultimately goes.

Modern Pricing Infrastructure Built to Last

A modern pricing infrastructure that is built to last leads with business-led pricing enablement, standardized integration, end-to-end traceability, analytics, and a phased execution approach.

Carriers that invest in their pricing function are not just reducing technical debt or accelerating rate deployment. They are creating a pricing function that is genuinely capable of supporting the growth, profitability, and competitive positioning that modern P&C markets demand.

Ready to take the next step? Gain a practical perspective on technology transformation across the pricing and underwriting value chain in ValueMomentum’s on-demand webinar, AI Insider Insights: How Leading Insurers Are Transforming Underwriting with AI.