Rising indemnity costs, increasing claim severity, and growing customer expectations are placing new demands on every stage of the claims life cycle. Claims function leaders are under pressure to improve accuracy, reduce cycle times, and strengthen the adjuster and policyholder experience, all while navigating legacy systems and fragmented workflows.

According to ValueMomentum’s claims maturity benchmarking study, some claims organizations have made meaningful advances in automation, digital engagement, and analytics, while others are still early in their journey, constrained by outdated processes or inconsistent adoption across teams and lines of business.

Modern pressures aren’t impacting all insurers equally, however. The differences come down to a handful of core elements that power the processes behind a claims organization’s overall performance.

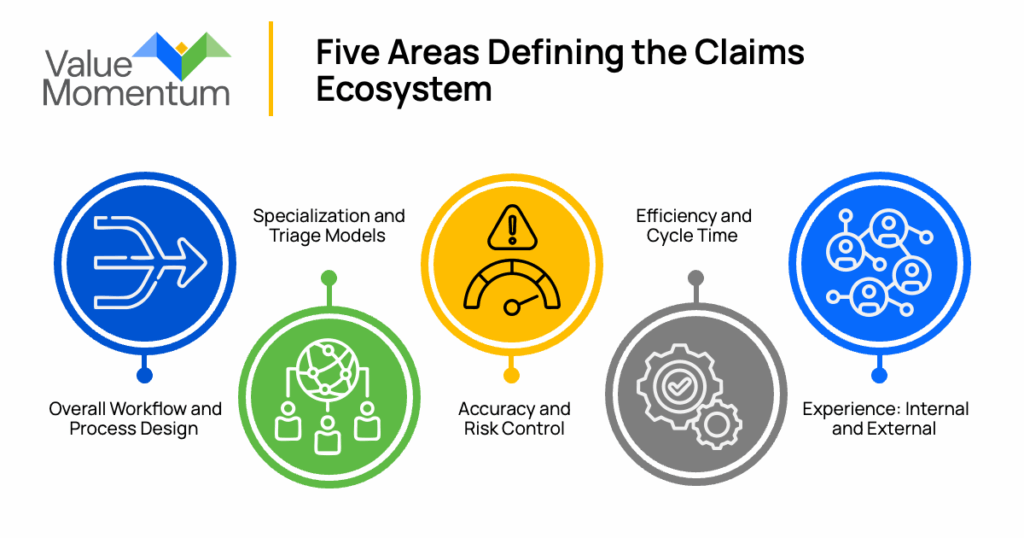

Five Areas Defining the Claims Ecosystem

As claim complexity grows, insurers are rethinking each step of the claims journey. While rising settlement values and social inflation push costs higher, even modest improvements in efficiency, accuracy, or oversight can translate into meaningful financial benefits.

Within this environment, a handful of key areas consistently determine how effectively insurers can respond. These components shape accuracy, efficiency, and customer outcomes, and ultimately define where a claims organization sits on the maturity spectrum.

1. Overall Workflow and Process Design

The structure of a claims operation largely determines how efficiently and consistently work moves from first notice of loss (FNOL) through settlement. Carriers relying on manual steps, fragmented tools, or paper-heavy processes often face delays, errors, and uneven execution. Mature organizations design streamlined, end-to-end workflows that support automation, improve hand-offs, and reduce bottlenecks, enabling claims to progress with greater clarity and speed.

2. Specialization and Triage Models

Traditional “everyone handles everything” models strain adjusters and can lead to misaligned resources. In contrast, modern carriers use intelligent segmentation and triage to match claims with the right level of expertise, routing simple claims through fast, automated paths and assigning complex or high-severity claims to specialized adjusters. This ensures effort aligns with complexity and improves overall outcomes.

3. Accuracy and Risk Control

Organizations that struggle with fragmented systems or limited data access often experience higher error rates and more leakage. Mature carriers, on the other hand, strengthen accuracy by integrating data, applying advanced analytics to decision points, and creating standardized validation steps that reduce variation and support more defensible outcomes.

4. Efficiency and Cycle Time

Processes weighed down by manual reviews, duplicated effort, or inconsistent routing tend to create long cycle times and higher workloads for adjusters. By streamlining tasks, automating repetitive steps, and aligning work across teams, modern carriers reduce operational friction and create capacity for higher-value activities, improving both speed and quality.

5. Experience: Internal and External

The claims experience impacts everyone involved, including not only policyholders and adjusters, but also their supporting teams. For customers, ease of communication, clear expectations, and fast updates shape trust and satisfaction. But internally, the adjuster experience matters just as much: intuitive tools, straightforward workflows, and fewer manual tasks improve productivity and reduce burnout. Organizations that elevate both sides of the experience ultimately improve performance, retention, and long-term loyalty.

Each of these areas plays a distinct role in shaping claims performance, influencing everything from operational accuracy to customer experience. When carriers focus on the underlying workflow, specialization models, accuracy controls, efficiency levers, and experience layers, the entire claims organization feels the impact.

Performance across these dimensions varies widely among insurers. How do large, midsize, and smaller carriers compare in their maturity journey, and what do those differences mean for their ability to modernize?

Where Insurers Stand in Their Maturity Journey

Claims transformation is underway across the industry, but the pace and depth of progress differ widely across carrier segments. Insurers are making meaningful advances, yet modernization remains uneven due to variations in budget, scale, system complexity, and digital readiness.

Here’s how maturity levels generally break down across large, midsize, and smaller carriers:

Large Carriers (Tier 1)

Large carriers tend to be further along in their modernization journey, supported by higher technology and operations investment. Many allocate 5.1–7.5% of total revenue toward technology and operations budgets and dedicate a significant portion of that to claims, often 11–20% of the enterprise tech budget, the highest share among all tiers.

This stronger investment position enables higher adoption of digital and AI-enabled workflows. Large carriers are more likely to have a greater percentage of claims processes fully digital or supported by intelligence-assisted automation. While this group still faces legacy complexity and variation across business lines, its scale enables broader pilot programs and more aggressive modernization initiatives, making Tier 1 carriers the most advanced segment overall.

Midsize Carriers (Tier 2)

Midsize carriers show steady progress but remain constrained by tightly integrated legacy systems and moderate technology budgets. These organizations generally invest 2.6–5% of total revenue in technology and operations — enough to make meaningful modernization gains but not enough to pursue sweeping transformation.

This dynamic pushes Tier 2 carriers to prioritize modernization in the areas that yield the greatest impact. The study shows that 44% of midsize carriers cite improving claims handling quality and efficiency as their top priority, while more than one-quarter focus on transforming their operating model and reducing loss adjustment expenses. Their adoption of digital workflows and AI-assisted processes typically falls in the mid-range, reflecting a targeted rather than enterprise-wide modernization approach.

Smaller Carriers (Tier 3)

Smaller carriers face the steepest modernization obstacles. These organizations often operate with the lowest technology investment capacity, typically at the bottom end of the 2.6–5% revenue range, and are the most likely to rely on outdated or fragmented systems that limit automation, integration, and data visibility.

The study shows that smaller carriers tend to have the lowest levels of digital workflow adoption and AI-enabled processes, underscoring their early position on the maturity curve. As a result, modernization efforts for Tier 3 carriers often begin with foundational improvements: digitizing intake, standardizing workflows, enhancing data quality, and adopting modular platforms that can be implemented incrementally without significant disruption or cost.

Differences across large, midsize, and smaller carriers highlight how claims modernization pressures manifest in distinct ways. Some organizations have the scale to invest heavily, while others must take a more incremental approach. But across segments, one theme is consistent: Maturity is not static. It’s shaped by how effectively carriers strengthen workflows, improve accuracy, streamline operations, and elevate the overall claims experience.

Preparing for the Next Phase of Claims Modernization

The claims ecosystem is evolving quickly, and each carrier’s maturity level reflects different strengths, constraints, and modernization paths. What matters most is an organization’s ability to clearly identify its current position and concentrate on the areas that will deliver the greatest operational and customer impact.

With a more accurate view of their ecosystem, insurers can make better-informed decisions about where to invest next and how to elevate performance across the claims life cycle.

Ready to move forward on your claims maturity journey? Read our report The State of Claims Maturity in P&C Insurance 2026 to learn how your organization measures up and how it can enhance its claims modernization.