Underwriters are running out of time to drive profitable growth while maintaining risk discipline.

As cyber threats, climate risks and other complex exposures grow, traditional underwriting is struggling to keep pace. For insurers, the risk isn’t just missed opportunities; it’s irrelevance in a market that demands speed, precision and deeper insight.

But a more adaptive model is emerging. Augmented underwriting combines human judgement with artificial intelligence, machine learning and real-time data to transform how risks are evaluated, priced and managed. In the UK commercial and specialty market, it is already streamlining triage, automating routine tasks and enriching risk understanding to meet rising expectations.

Clients want more than protection. They expect timely, practical guidance on how to build resilience and proactively prevent loss. Insurers can deliver on that promise; implementing augmented underwriting can deliver real value.

The practical gains

Today, underwriters spend nearly half their time on data administration. Augmented tools are starting to change that. Artificial intelligence (AI) assistants scan submissions, enrich them with third-party data, apply risk appetite underwriting rules and generate risk scores within minutes, helping underwriters evaluate submissions more efficiently and effectively as well as identify where to quote, where to decline and where to compete.

Routine cases are handled automatically, while high-risk ones trigger structured data requests to brokers. This improves speed of response to brokers, accelerates throughput, reduces cost and allows underwriters to focus on complex risks and client advisory conversations.

Consider a global logistics client seeking P&C coverage for 50 warehouses across five countries. Traditionally, underwriting this risk would take weeks of manual work. With augmented underwriting, AI draws on live data, such as satellite imagery, Internet of Things (IoT) feeds, crime statistics and climate risks, while generative AI (GenAI) summarises claims history and regulatory context. Advanced analytics highlight hidden exposures. The underwriter reviews the insights, applies judgement and delivers a tailored quote in just a few days.

While this example focuses on the insurer, the benefits reach further. Brokers gain from faster responses and clearer insight, while clients receive coverage aligned to live risk profiles, which is crucial in areas like cyber or property catastrophe where delays can leave underinsured gaps.

Proof points from the market

Augmented underwriting has shifted from trial to boardroom priority. KPMG’s 2024 Insurance CEO Outlook found that 81 percent of global insurance CEOs consider GenAI to be a top investment priority.

The question is no longer if but how firms apply it to deliver value. The applications are many:

- Ki Insurance, part of Brit Insurance at Lloyd’s, is simplifying and speeding up how brokers assess risks. Its platform offers instant quotes, cutting placement timelines from weeks to minutes and making it faster and easier for brokers to secure cover for their clients.

- AEGIS London is advancing algorithmic follow-only underwriting with Opal, its proprietary platform that automates the process, allowing insurers to join others in covering a share of a policy rather than leading it. Drawing on rich data sets, Opal automates risk selection, enabling scaled follow strategies that were once limited by manual processes.

- In 2024, Hiscox partnered with Google Cloud to launch GenAI-enhanced underwriting for sabotage and terrorism, cutting quote times from days to minutes. Hiscox has also embedded AI into cyber and professional indemnity underwriting for small and medium enterprises (SMEs). While technology is accelerating change, it can’t replace the fundamentals. As Hiscox CEO Aki Hussain put it, “We’ve built the chassis; the trust [from the underwriters] is now coming through.”

- Brokers are also taking a leading role. McGill and Partners’ Auton platform provides automated risk selection through a bespoke rules engine developed in partnership with Verisk. This signals a shift in broker value from pure intermediation to intelligent risk curation and data-driven decision-making.

What could be the downside?

Data quality remains the biggest brake. AI models need clean, consistent inputs, yet many insurers still rely on fragmented systems. Only 18 percent have fully migrated to the cloud, according to KPMG’s 2025 Global Intelligent Insurance Report, though 60 percent cite partial progress.

As one UK insurance CIO expressed in the report, “We have legacy infrastructure and applications. We have silos, and we need to do more work with our data to ensure it is clean and accurate.” For augmented underwriting to scale, these gaps must be closed.

Even with cleaner inputs, insurers must trace and justify every AI-driven decision. Transparency is now a regulatory imperative, essential not just for compliance, but to sustain trust with brokers and clients. Insurance organisations must set clear baselines for accountability, fairness, transparency and other essential practices in the responsible use of AI.

What’s next

As AI matures, UK insurers are moving from operations automation to business transformation. Portfolio underwriting and digital risk exchanges promise greater speed, scale and strategic control. But this shift goes beyond efficiency. It positions insurers as risk partners, using deeper insights to help clients build resilience, manage under insurance from flood protection to cyber security.

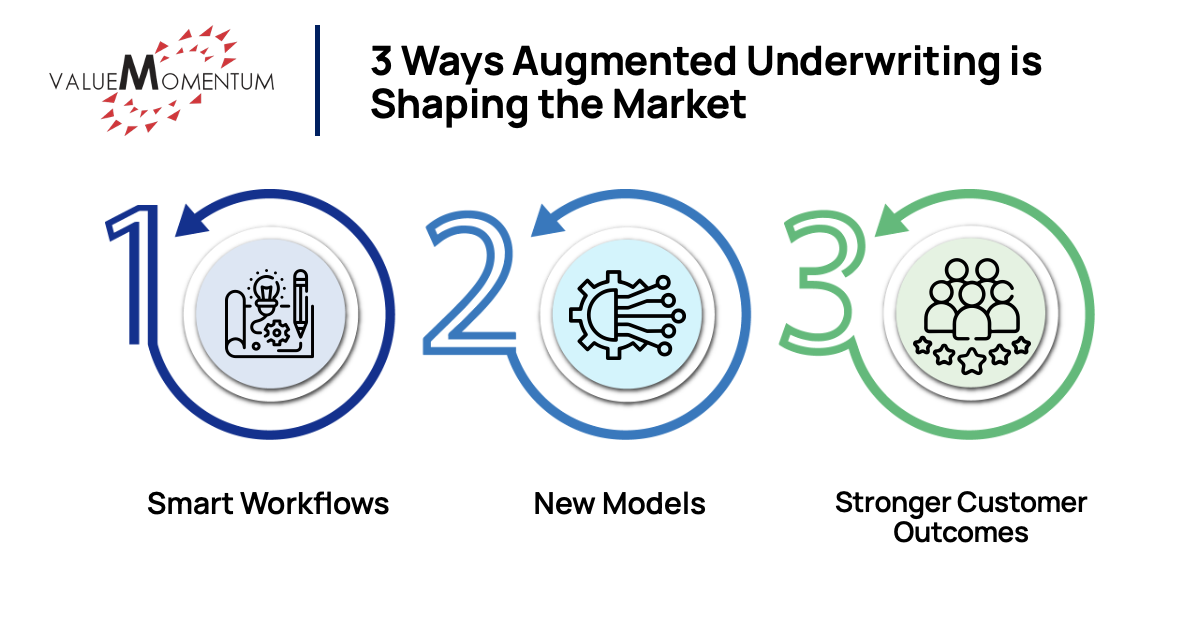

This evolution is playing out in three primary ways as augmented underwriting reshapes the market:

- Smarter workflows. This reinforces a key theme so far: The greatest potential lies in day-to-day operations. According to EY-Parthenon’s 2024 Global GenAI Report, 58 percent of insurers expect GenAI to automate over 60 percent of underwriting and operations within five years. Routine cases can be handled automatically, boosting throughput, cutting costs and improving consistency.

- New models. As AI underwriting assistants mature, insurers can unlock new business models to drive scalable, profitable growth. Underwriters could shift to portfolio-level oversight, with AI handling individual risk trades. Others may offer digital risk exchanges that automate risk-capital matching and enable auction-style underwriting decisions.

- Stronger customer outcomes. With AI-driven analytics, underwriters can offer more tailored advice to help customers improve their risk profiles, such as strengthening flood protection or bolstering cyber defences. This supports greater resilience to emerging risks and helps address underinsurance as rising costs push some to reduce or forgo essential cover.

Augmented underwriting is fast becoming the norm. Combining human judgement with AI brings real gains in speed, scale and accuracy. But success depends on more than smart tech. It requires clean data, transparent models, strong oversight and close collaboration between insurers, technology partners, data providers and regulators.

Those who get it right will not just move faster but reshape how risk is understood and delivered. And just like the data, the value delivered will depend on the input.

Learn more about how one insurer enhanced its underwriting process in our case study, “Midwestern Specialty Insurer Optimises Submission and Forms Process With Application Engineering”.