Underwriting has always been central to insurance — but many insurers still rely on manual processes, static rules, and outdated scoring models. These legacy workflows slow decisions and limit insurers’ abilities to respond to emerging risks like climate volatility and cyber threats.

In fact, Canadian managing general agents (MGAs) and insurers may be missing up to 50% of broker submissions due to incompatible data formats, with key risk information often shared in PDFs, Word documents, and even handwritten notes. To stay competitive in an increasingly complex world, insurers need more adaptive solutions.

That’s where agentic AI comes in. These intelligent, autonomous systems continuously ingest real-time data, refine risk models, and make decisions with minimal human input. Unlike traditional automation, agentic AI incorporates feedback loops, learning from past outcomes to continuously improve.

How Agentic AI Enhances Underwriting

Traditional AI helps automate underwriting, but it’s limited by static decision trees and infrequent model updates. Agentic AI is goal-driven, context-aware, and self-improving—delivering smarter, more responsive underwriting at scale. Automating with agentic AI can help insurers cut turnaround times from weeks to minutes.

Agentic systems pull from Internet of Things (IoT) devices, financial records, and regulatory sources to detect fraud and ensure compliance. They also evolve with new risks without needing manual reprogramming. In short, while traditional AI supports underwriting, agentic AI transforms it in collaboration with human experts.

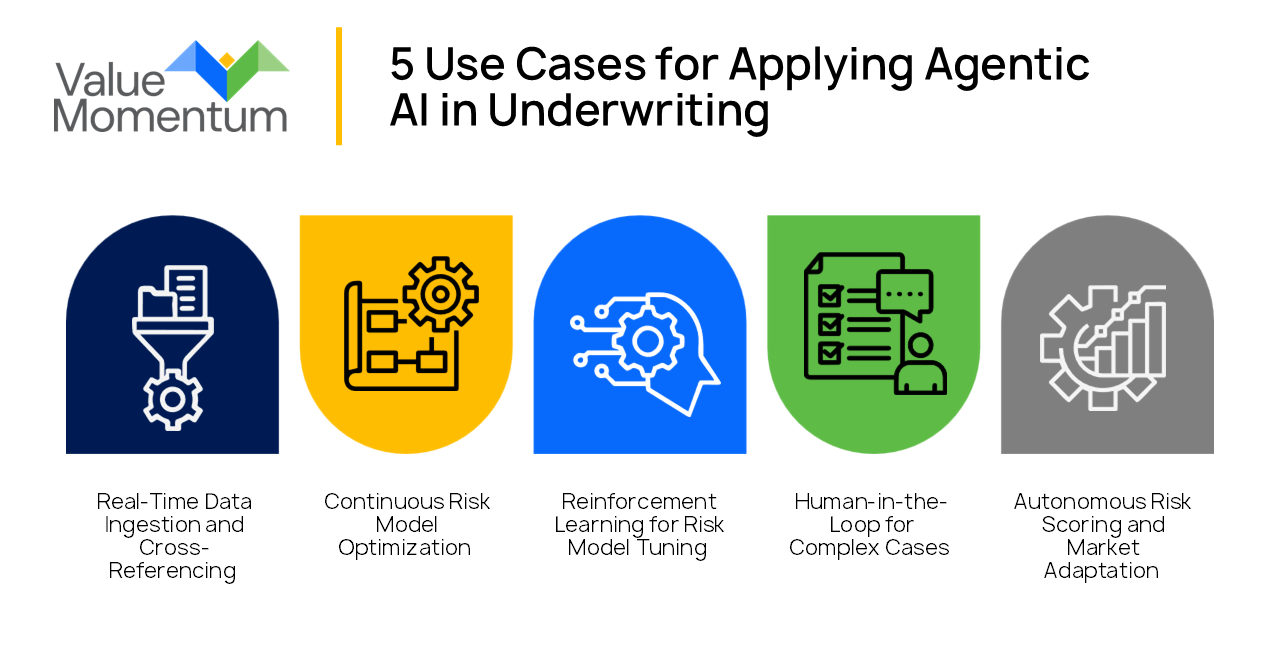

These tools are already capable of summarizing documents, reviewing underwriting guidelines, and pulling expert opinions out of troves of unstructured data. But what does the future of agentic AI look like? Here are five real-world use cases for applying agentic AI to transform underwriting:

1. Real-Time Data Ingestion and Cross-Referencing

Agentic AI systems elevate underwriting accuracy by continuously ingesting and synthesizing structured and unstructured data in real time. These systems pull from a wide range of sources to create a comprehensive view of risk, including:

- Public records and regulatory data for verifying applicant identity and compliance.

- IoT and telematics for behavioral risk assessment and real-world usage patterns.

- Social media and digital footprints to flag fraud indicators and inconsistencies.

- Third-party financial and credit data to assess solvency and financial behavior.

By cross-referencing these inputs, agentic systems build a dynamic, 360-degree risk profile, which is far more nuanced and timely than what traditional models offer. For example, using AI agents to automate 93% of its data aggregation, a US-based agricultural insurer dropped its average underwriting process time by 82%. These efforts also led to a 7% rise in the insurer’s NPS.

2. Continuous Risk Model Optimization

Unlike static risk models, agentic AI systems dynamically refine their assessments through continuous learning and adaptation. Machine learning algorithms analyze historical claims data to identify patterns and adjust risk factors accordingly, while generative AI (GenAI) simulations explore various underwriting scenarios, predicting potential outcomes and informing decision-making.

In addition, predictive analytics estimate future claim probabilities, enabling proactive risk management. An agentic system could see trends in markets occurring and tweak the risk models before a crash happens, such as an epidemic increasing the cost of goods.

In the financial services space, Moody’s has started leveraging a multi-agent system to compare the financial risk of companies across parameters; similar logic could be leveraged in insurance.

3. Reinforcement Learning for Risk Model Tuning

The reinforcement learning (RL) used in agentic AI helps improve underwriting decisions based on outcomes, enabling the system to learn not just from patterns, but from experience. According to a study published in the African Journal of Artificial Intelligence and Sustainable Development, these RL models have dynamically adjusted to market shifts and evolving risk profiles before, resulting in more responsive strategies that outperformed static models in risk and capital efficiency.

RL algorithms allow agentic systems to explore a range of risk evaluation strategies and prioritize those that produce more favorable results, such as reduced claim severity or improved profitability. With each underwriting decision, the system evaluates what worked and what didn’t, then it updates its approach accordingly.

Arch Insurance, for example, has leveraged Kalepa’s Underwriting Copilot to help bring submissions aligned with the insurer’s risk appetite criteria to underwriters’ attention, as well as tracking whether a submission will help the insurer reach its portfolio objectives. The system has helped Arch nearly double how many submissions its underwriters review daily.

4. Human-in-the-Loop for Complex Cases

Zurich Insurance, in collaboration with the University of Technology Sydney, implemented AI tools to expedite life insurance application processing, particularly those involving mental health disclosures. While the AI analyzes extensive data to streamline assessments, human underwriters review and validate the final decisions, ensuring accuracy and empathy in sensitive cases. This hybrid approach reduced processing times from 22 days to less than a day.

Similar approaches could be used across P&C lines of business. Agentic AI systems excel at automating routine underwriting tasks, but human expertise remains crucial for handling complex or ambiguous cases. By incorporating human judgment into the AI loop, insurers can ensure nuanced decision-making and maintain accountability.

Feedback from human interventions is used to retrain and refine these AI models, enhancing their performance over time. On top of ensuring nuance remains part of the process, keeping humans involved in decision-making processes ensures compliance with regulatory standards and fosters trust among stakeholders.

5. Autonomous Risk Scoring and Market Adaptation

Agentic AI systems autonomously adjust risk assessments in real time, responding to both internal data and external market dynamics. This capability ensures that underwriting decisions remain accurate and relevant in a rapidly changing environment. Agentic AI continuously updates risk scores by analyzing internal claims data alongside external factors such as economic indicators and emerging threats.

By monitoring real-time market conditions, agentic AI adjusts underwriting strategies to align with current trends, ensuring competitiveness and profitability. The integration of diverse data sources allows for more nuanced risk segmentation, leading to better pricing strategies and reduced underwriting uncertainty. And by autonomously adapting to changes, agentic AI systems can help insurers maintain accurate and efficient underwriting processes.

One European insurer leveraged DRUID’s AI agent, CLARA, to provide self-service travel insurance to customers 24/7. Customers can select the policy appropriate to their situation, scan their ID to verify their identity, and pay online in less than 10 minutes. The platform independently assesses the risk of each submission and issues the policy, which has led to a 20% increase in contracts signed.

Together, these capabilities demonstrate how agentic AI moves underwriting from a static process to a dynamic, continuously improving system — setting the stage for what’s next.

The Next Generation of Risk Assessment

Underwriting is at a turning point. Traditional risk assessment models, constrained by manual processes and static data, can no longer keep pace with the digital world. Agentic AI offers a smarter, more adaptive approach, using real-time data and continuous learning to enhance accuracy and speed.

For insurers, the payoff is clear: faster underwriting, better risk selection, fewer surprises, and greater resilience. Those who move now will lead the way in a new era of intelligent, data-driven underwriting.

Interested in learning more about AI’s impact on insurance? Download our e-book, “The History of AI in Insurance and Where It’s Headed.”